On March 10th, 2023, Silicon Valley Bank (SVB) was placed under the control of the Federal Deposit Insurance Corporation (FDIC) following a bank run that left it unable to return all of its customers’ deposits. A worrisome contingency involving the liquidity of the bank’s assets quickly evolved into the second-largest bank collapse in US history and the most significant financial crisis since 2008, with the cost of the bank’s collapse estimated at nearly $20bn.

At the onset of the inflationary period in 2022, the Federal Reserve began raising interest rates to combat rising prices. This was a problem for Silicon Valley Bank since most of its assets were held in the form of government bonds and treasuries, whose value naturally falls when interest rates are increased. The bank did not hold short-term investments to act as buffers for liabilities, therefore losing all liquidity due to not wanting to sell bonds for a significant loss. However, once startup clients began withdrawing deposits during a volatile period for companies and fundraising, there was a shortage of cash available to be returned. SVB found itself in a position where it needed to sell off its bonds, and it did so at a staggering $1.8bn loss.

By the end of March 9th, clients withdrew $42bn of deposits. This did not seem alarming to the bank, however, as it ensured consumers that the situation was under control. The following morning, the FDIC stepped in and Silicon Valley Bank ceased to exist.

SVB had in its possession assets collectively worth around $209bn at the end of 2022, according to the FDIC. The bank provided financing for companies more on the unstable side, unlike some other big banks. Many of its depositors were startups that had deposited large amounts of money due to the high demand for their products during the pandemic.

On March 26th, the FDIC announced that Silicon Valley Bank would be purchased by First Citizens Bank, which would take control of the majority of the leftover deposits and loans. Under this takeover deal, all 17 branches of SVB opened under the First Citizens Brand. The North Carolina-based bank bought around $72bn of SVB’s assets at a heavily discounted price of $16.5bn, making itself one of the 25 largest banks in the United States.

The next piece in the line of financially unstable dominoes was Signature Bank, which fell soon after Silicon Valley Bank’s collapse. After seeing SVB’s failed attempt at raising capital and paying clients back, customers of Signature Bank withdrew $10bn on March 10th. On the same day, the bank’s stock experienced the greatest drop since it went public in 2004 – a drop of 23%. According to board member Barney Frank, clients moved their deposits to bigger banks such as JP Morgan and Citigroup. Two days later, the FDIC shuttered Signature Bank, and it met the same fate as SVB, in what was the third-largest bank failure in US history.

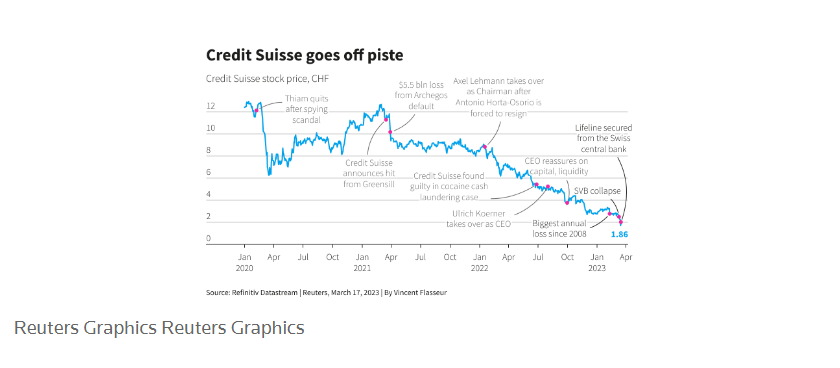

Finally, the third and most recent bank failure comes from across the Atlantic Ocean, with Credit Suisse which was recently bought by rival Swiss bank UBS for around $3.3bn. This bank collapse differs from the others in the way that it was caused by the bank’s poor decision-making and scandals rather than a wider economic scenario. Ex-CEO Tidjane Thiam resigned in February 2020, after a 2019 spying scandal. Chairman Antonio Horta-Osorio left the bank in January 2022, following an issue regarding his breach of Swiss and British COVID-19 quarantine protocols. These two incidents all played a part in creating an atmosphere of mistrust around the bank, with clients suspicious of illegal operations. In July 2022, Credit Suisse’s new CEO revealed a strategic review that failed to convince shareholders to be optimistic about the situation. A rumor about an impending failure of the bank spread and caused a mass exodus of customers.

In March 2021, Credit Suisse’s cooperation with Greensill Capital failed, forcing the Swiss bank to close a $10bn group of funds. A few weeks later, the collapse of Archegos Capital caused a further loss of $5.5bn to the bank. An independent report later claimed there was a “fundamental failure of management and controls” and a “lackadaisical attitude towards risk” from Credit Suisse’s side.

At the end of 2021, Credit Suisse had AUM (Assets under management) worth 1.6 trillion CHF (around $1.75 trillion USD). This amount dropped to 1.3 trillion CHF a year later, and on March 14th, 2023, the bank stated it had identified “material weakness” in its controls over financial reporting. Three days later, the Swiss National Bank agreed to offer $54bn to help the bank stay on its feet, but soon after UBS swooped in and bought the second-largest bank in Switzerland.

Based on these bank collapses, coupled with all other major economic events, it is easy to say that the financial world is currently staring at an unstable future. In the near future, the deposits of these banks will be returned and the debts will be paid but the question remains: will this trigger a wider financial crisis across the world?

{kind=link}