There is probably a risk of becoming monotonous, but much of the explanation for the movement in the financial markets in recent weeks revolves around the theme of inflation. And when it comes to financial markets, one cannot fail to start with the situation in the USA.

As the ancient thinkers would have claimed, we need to start from the assumption. What is the thesis that supports the recovery of the financial markets in recent weeks? That inflation in the US, after raging in 2022, will drop rapidly in the year that has just begun. This is a premise that emerges clearly by analysing the trend of some indicators, starting from the difference in yield between non-indexed and indexed government bonds. The break-even inflation rate deriving from the comparison between Treasuries maturing January 2024 and TIPS (government bonds linked to inflation) of the same duration has fallen to 2.7% in recent weeks. In other words, it means that investors expect US inflation to drop quite quickly, with a return to the 2% area within 12 months.

Even observing the inflation trend expectations elaborated by the Federal Reserve Bank of Cleveland (which includes in the calculation, in addition to the break-even, also the so-called inflation swaps and polls) it is noted that from the peak of 4.22% last June 2022, the 12-month inflation expectation is around 2.66% today.

Small statistical parenthesis. Considering that the inflation rate was above 9% at its peak, the expected drop by January 2024 would be more than seven percentage points. To trace such a rapid decline in US inflation we need to go back to the dark times of the 2008 recession and to the period of super restrictive monetary policy adopted by Volcker in the 80s of the last century.

Even in light of this small statistical note, what does this thesis support? According to many analysts, investors seem convinced that by this summer the costs of many raw materials, energy first and foremost, will undergo a sharp reduction, dragging down the rest of the basket as well. However, there is also another version, much less comforting: the arrival of a powerful recession capable of “spreading the legs” of demand and triggering a consistent deflationary phase. An eventuality that, given the trend of the markets in recent weeks, does not seem to be taken into great consideration.

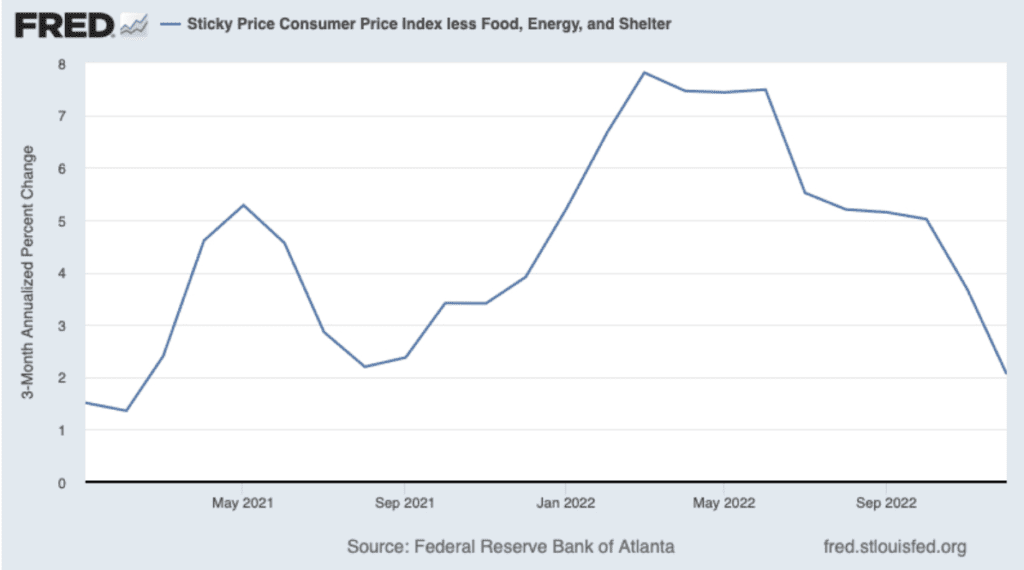

But beyond expectations, is inflation really going down? One of the most relevant indicators in this sense is that relating to the trend of the so-called sticky prices, which tend to move only and exclusively if there are very good reasons to do so.

The chart above, a core version of the Sticky Price Index, without the more volatile components of the basket, would suggest that a downward movement is underway from the peaks of the first half of 2022.

In short, the initial hypothesis of a rapid drop in inflation in the US seems to have foundations in the macro data, even if quantifying how much inflation will fall is rather daring. As noted by some analysts, it is more plausible to hypothesise a return to 4% within 12 months, an element that would imply at the moment the presence of an excessive dose of optimism on the part of investors. An excess makes the path of stock lists much more uncertain in the coming months.

Featured image: Unsplash

{kind=link}